GRS Unleashed: The modern advisor's guide to group retirement

to date

business

How many group retirement plans have you personally placed or led?

Topics and areas you hope to cover today

What we'll cover today

The Market & Opportunity

Everything you need to know about Canada's retirement landscape, group plan types, and why this is one of the fastest-growing opportunities in financial services.

The Retirement System

Canada's three-pillar framework, CPP & OAS basics, and the retirement readiness gap that creates massive opportunity.

The Market

A $365.6B industry with 83,000+ plans. Plan types, regulatory landscape, and competitive positioning.

The Opportunity

Why group retirement is a great business for advisors — recurring revenue, compounding AUA, and underserved SMBs.

The main goal of retirement finance sounds simple

Maintain your standard of living after full-time work ends.

Most Canadians get retirement income from multiple sources

And maybe also...

Canada's retirement income system

Canada's retirement security rests on three pillars — but two of them were never designed to fully replace working income. That's where advisors come in.

CPP & OAS in 2026

| Benefit | Typical | Maximum |

|---|---|---|

| Canada Pension Plan (CPP) | ~$10K/year | ~$18K/year |

| Old Age Security (OAS) | ~$9K/year (max) | |

| Total typical government benefits | ~$19K/year | |

CPP Enhancement

~50% of the CPP enhancement is phased in — won't be fully phased in until 2065

CPP Contributions

Max member & employer CPP contribution: ~$4,600 each per year

OAS Spending

OAS is Canada's most expensive public program — 17% of federal spending

Canadians are not ready for retirement

Millions of Canadians are underprepared for retirement — and the gap is widening.

Confidence gap

Workplace plans raise retirement confidence by 25 percentage points.

The massive coverage gap

Public vs. Private Sector

Canada vs. the U.S.

Why employers set up workplace retirement plans

A workplace plan isn't just good for employees — it's a strategic business decision with measurable ROI.

Rated by employers as the number one recruitment tool — a workplace retirement plan is the benefit most likely to attract top talent, especially in competitive SMB markets.

Workplace plans can reduce employee turnover by 20-60%. Given that the cost of replacing an employee runs 20%-100% of their salary, the savings add up fast.

The estimated cost of employee financial stress per employee per year. A retirement plan is one of the most effective ways to reduce it — improving focus, productivity, and engagement.

The basics of retirement math

The replacement ratio

Financial planners typically recommend replacing 60-80% of pre-retirement income. For someone earning $75,000:

The gap of ~$26K-$41K/year must come from workplace plans and personal savings — that's roughly $600K-$1M in retirement savings. That's the advisor opportunity.

Why starting early matters

The power of compounding on a $500/month contribution:

Group retirement is a $350B+ market — and growing

$365.6B CAP market breakdown

Top 9 CAP market grew 16.8% YoY — Benefits Canada 2025 CAP Suppliers Report

CAP = registered Capital Accumulation Plans (Group RRSP, DC, DPSP, EPSP). Excludes individual insurance-based group RRSP solutions.

Key growth drivers

- SMB coverage gap closing through advisor-driven distribution and fintech innovation

- Employer competition for talent driving benefits adoption

- Regulatory evolution (CAPSA 2024 update, potential auto-enrollment)

- Shift from DB to DC in private sector

- Financial wellness as an HR priority

Key plan types for advisors

| Plan Type | Tax Treatment | Employer Match | Vesting | Best For |

|---|---|---|---|---|

| Group RRSP | Pre-tax; taxed on withdrawal | Optional | Immediate | Most common starter plan for SMBs |

| Deferred Profit-Sharing Plan (DPSP) | Employer-only; taxed on withdrawal | Employer only | Up to 2 years | Retention tool — paired with Group RRSP |

| Group TFSA | After-tax; tax-free growth & withdrawal | Optional | Immediate | Flexibility; lower-income; complement to RRSP |

| DC Pension | Pre-tax; locked-in until retirement | Required | Varies by province | Strongest governance; pension legislation applies |

CAPSA CAP Guidelines — Updated 2024

The first major revision in 20 years signals a fundamental shift. Four themes define the new direction:

1. Outcomes, not just options

The old guidelines focused on giving members investment choices. The 2024 update shifts to retirement income adequacy — sponsors must consider whether their plan actually helps members retire well.

2. Ongoing education and planning

Sponsors should provide members with retirement income projections, financial planning tools, and access to professional advice — not just fund fact sheets. Education is now a continuous responsibility.

3. Stronger governance

Plan sponsors must regularly review investment options, fees, and member outcomes. Governance is no longer a set-it-and-forget-it obligation — it requires ongoing attention and expert support.

4. Focus on value for money

New emphasis on ensuring fees are reasonable relative to services provided. Sponsors must demonstrate that members are getting real value from their plan — raising the bar for all providers.

Why this is a massive opportunity for advisors

- Employers need expert guidance to meet new governance standards

- Plan sponsors must now review investment options, fees, and member outcomes regularly

- The shift to outcomes-based thinking creates ongoing advisory relationships, not one-time sales

- Advisors become the compliance bridge between regulators and small employers

The competitive landscape

The Big 3 dominate the CAP market

More than 80% of all CAP assets are held by just three carriers:

Source: Benefits Canada 2025 CAP Suppliers Report (as of June 30, 2025)

The Common Wealth difference

- Purpose-built for SMBs — no minimums, fast onboarding

- Modern full-stack technology platform

- Accessible to all advisors, not just longtime specialists

- Specialized: group retirement is all we do

Group plans deliver better outcomes than retail

Workplace retirement plans consistently outperform individual retail arrangements across every dimension that matters.

Lower fees

Group plans leverage pooled buying power to access institutional-grade investments at a fraction of the cost of retail mutual funds — often 50%+ lower MERs.

Education and planning

Group plans provide built-in financial education, retirement projections, and planning tools that members wouldn't seek out on their own.

Payroll-based savings

Automatic payroll deductions make saving effortless. Members don't have to remember to contribute — it happens every pay cycle, building the savings habit by default.

Stronger oversight

Fiduciary governance, regulated investment menus, and professional fund selection — members benefit from expert oversight they wouldn't get managing savings alone.

Yet 80%+ of Canadians' retirement savings sit outside of group plans — in retail RRSPs, TFSAs, and non-registered accounts — despite group plans being more efficient. That's a massive opportunity to move savings into a better structure.

Key trends shaping the market

Digital experience & engagement

Members expect mobile access, real-time projections, and seamless digital enrollment. Platforms that drive engagement lead to better savings outcomes — and stickier plans.

Financial wellness and education

42% of Canadians say money is their #1 stress. Employers are increasingly looking for plans that include financial wellness tools and education — not just an investment account.

Simpler fund line-ups

The era of 50+ fund menus is fading. Best practice is now curated, streamlined investment options with strong defaults — target-date funds, balanced portfolios, and auto-features that help members without overwhelming them.

Financial planning & advice

Plans are moving beyond investment menus to include retirement income projections, goal-setting tools, and access to professional advice. The new CAP guidelines reinforce this shift.

Why group retirement is a great business for advisors

Contribution-based commissions arrive with every payroll cycle. Unlike one-time insurance sales, your income is steady, predictable, and plannable.

As assets grow through contributions + market returns, your AUA-based revenue grows too. A well-built book compounds year over year — even without adding new plans.

Group retirement gives you a seat at the table with the business owner and HR. It opens doors to benefits cross-sell, individual financial planning, and a trusted-advisor role.

Plans rarely move once set up. Average plan tenure is 7+ years. The switching cost is high and the relationship deepens over time — making your book highly durable.

Book-of-business growth calculator

See how your group retirement book compounds over time. Adjust the inputs to model your own growth trajectory.

Cumulative AUA

●Annual Revenue

The opportunity is enormous

- 9.1 million Canadians lack a workplace retirement plan — this is a solvable problem

- Government benefits alone replace less than 40% of income for most workers

- Group retirement is sticky, recurring, compounding revenue for advisors

- Modern platforms like Common Wealth have removed the historical barriers for SMBs

- The regulatory environment is moving toward better retirement outcomes, not just investment options

Sales & Set-Up

How to prospect, pitch, and onboard new group retirement plan clients — from first conversation to first payroll contribution.

The Buying Landscape

How CAP guidelines created new conversations, what's changing in the buyer journey, and who's actually making the decision.

Plans in Motion

Displacements, trigger events, and how to identify employers who are ready to act — even if they don't know it yet.

Overcoming Obstacles

The real barriers to a closed plan — and the frameworks, language, and data to address each one.

Three trends in employer expectations and the GRS market

1. Member engagement is the new frontier

Increasing focus on member engagement and opportunities to add value at the individual member level. This is a chance for advisors to future-proof their model by going beyond plan setup to ongoing member outcomes.

2. The advisor's role in expanding coverage

Getting employers over the hump to set up a plan — most won't do it on their own. The industry is shifting from "my job is service" to a growth orientation: increasing block penetration, building effective go-to-market, and figuring out how to sell GRS. There's a critical role for advisors in making that happen.

3. Employers want advice, not just quotes

Employers want help navigating the market: Are you using your plan effectively in your HR strategy? Are your people getting the help they need? This advisory role is far more valuable than being a pure broker collecting quotes.

Know your decision maker — it changes by company size

| Company Size | Key Decision Maker | What They Care About Most |

|---|---|---|

| 2–20 employees | Business owner (often the founder) | Cost, simplicity, and "will my team actually use it?" |

| 20–75 employees | Owner + HR generalist or office manager | Compliance peace-of-mind and ease of payroll integration |

| 75–250 employees | HR director (influencer) + CFO (approver) | Competitive benchmarking, total comp cost, and plan metrics |

| 250+ employees | Benefits committee + legal/finance sign-off | Fiduciary risk, investment menu governance, member outcomes |

Employers act when something triggers urgency

Most employers don't wake up thinking about group retirement. They act when something disrupts the status quo. Learn to recognize — and create — these moments.

Growth milestones

Hitting 10, 25, or 50 employees often prompts a benefits review. "We're scaling — what do our people need to stay?" is a natural door opener.

Talent loss / near-miss

A key employee leaves — or almost leaves — citing benefits. Nothing sharpens the mind of a business owner faster than an avoidable departure.

Competitor offering plans

An employer hears a competitor added a group RRSP. Or they lose a candidate to a company offering retirement benefits. Competition is a powerful motivator.

Tax season / year-end

Business owners thinking about their own tax bill often ask their accountant about group plans. Employer matching is deductible. DPSP contributions reduce payroll tax.

Employee requests

Employees asking for retirement benefits — especially in company surveys or 1:1s — put the issue directly on the owner's desk. Validate the ask and come with a solution.

Regulatory awareness

An employer reads about CAPSA 2024 or gets flagged by their accountant. They realize their existing plan or lack thereof has a compliance gap. This is your call.

How they buy

The advisors who win aren't just finding the right clients — they're running a faster, simpler process once the conversation starts.

The old way

- Formal RFP issued to multiple providers

- Weeks of comparison spreadsheets and paper brochures

- Multiple finalist presentations with large committees

- Long decision cycles with plenty of opportunities to stall

The new way

- Surface the need through a wellness or business conversation

- Move quickly to a live platform demo — show, don't tell

- Present a small number of benchmark-driven plan design options

- Give the decision-maker everything they need to say yes

How Common Wealth accelerates this

Proposals that close

Clean, visual proposals that are easy for employers to share internally and get fast sign-off.

Speedy pricing

Pricing quotes turned around quickly — and even faster with AI.

Momentum after the yes

Simple onboarding that keeps things moving once the employer is ready to go.

On-demand demos

Common Wealth joins advisor calls to deliver live client demos on demand — no prep required on your end.

Opportunities to improve existing plans

Low engagement

Many plan members take the employer match and disengage. A plan review can identify ways to increase participation, contribution rates, and overall member engagement.

Outdated fee structures

Some plans are still on fee schedules set years ago. As assets grow, fees should be reassessed to ensure members are getting fair value for what they pay.

Plan design issues

Over time, issues build up: members in unsuitable funds, outdated investment menus, or plan designs that no longer match the workforce. A review can surface these and recommend improvements.

Service gaps

Smaller employers without dedicated HR often don't get the support they need from legacy carriers. Modern providers can offer a better experience for both employers and members.

Existing plans are an underleveraged opportunity

Most Canadian SMBs with a group plan haven't reviewed it in years. The market is moving — advisors who engage existing plan holders are finding real opportunity.

Signs a plan is ready for a review conversation

- High administration fees with no fee benchmarking review in 3+ years

- Low member participation (<50%) — sign of poor enrollment and engagement

- No auto-enrollment, auto-escalation, or default investment options

- Legacy carrier platform with no mobile access or member projections

- Advisor is retiring, inactive, or simply absent from the relationship

- Employer has grown significantly since plan was set up — plan design hasn't kept up

How a displacement works

From the client's perspective, a plan transfer is simpler than it sounds.

Sign on

Plan design and matching levels typically stay the same. No big decisions required to get started.

Setup

Common Wealth handles it. Employer involvement is minimal.

Educate employees

Employees are informed about the change and why it benefits them — through sessions and employer communications.

Fresh enrollment

Every employee re-enrolls. An opportunity to re-engage, revisit contributions, and nudge good behaviors like maximizing the match.

Assets transfer

Common Wealth receives the file and cheque from the legacy provider. Funds deposit automatically, and anyone who didn't self-enroll is auto-enrolled.

The five objections you'll hear most — and how to answer them

"We're fine for now"

Most employers don't think about a plan until someone asks the right question. Bring it up at every meeting — the need is usually there, it just hasn't been surfaced yet.

"We can't afford it"

Employer contributions are completely flexible. Start with a modest match or a fixed dollar amount per employee. You're not committing to a big number — you're building something you can grow over time.

"Sounds like a lot of admin"

Modern platforms have dramatically reduced setup and admin time — what used to take months now takes days. Once the plan is running, ongoing admin is close to zero.

"We're too small"

Technology has lowered the bar significantly. A modern plan is just as easy for a 10-person company to run as a 200-person one. Size is no longer the barrier it once was.

"Why not just give employees a raise?"

A retirement plan gives employees something a raise can't. Contributions are tax-sheltered with no CPP or EI on the way in. Employees get access to low-cost investment funds, built-in financial planning support, and a powerful behavioural advantage — contributions come off the paycheque automatically before they can spend it. That combination is genuinely difficult to match with salary alone.

The real cost of a group retirement plan

Most employers overestimate the cost and underestimate the flexibility of a group retirement plan.

| Total employees | 50 |

| Participating employees | 35 |

| Avg salary | $65,000 |

| Employer match | 5% of salary |

| Total annual cost | $113,750 |

| Each participating employee receives | $3,250/yr |

| Match | Annual Cost | Monthly | Per Emp/mo |

|---|

Show, don't tell — a 10-minute demo closes more than an hour of pitching

Show, don't tell

Seeing the platform in action answers more questions in 2 minutes than a brochure does in 20. Employers understand what they're buying — and so do their employees.

Builds momentum fast

A live demo creates real interest and urgency. It answers "how does it work?", "why is it better?", and "how do we get started?" — all in one conversation.

Shows the employee experience

Employers care about whether their team will actually use the plan. The member-side experience — mobile app, projections, enrollment flow — is your strongest argument for participation.

The best advisors know the market

- Know your buyer — decision makers and priorities shift with company size

- Trigger events create urgency — growth milestones, talent loss, and benefits reviews open doors

- The old RFP process is giving way to faster, demo-driven sales — Common Wealth supports you at every step

- Existing plans are an underleveraged opportunity — most haven't been reviewed in years

- Objections are normal — the answers are straightforward when you know what's really behind them

Post-Implementation Success

The plan is live. Now the real work begins — keeping it healthy, building member trust, and growing your book.

The New Governance Model

From compliance checkboxes to genuine member outcomes — what good plan oversight looks like in 2026.

Metrics That Matter

What employers and advisors should be tracking — participation, engagement, retirement readiness, and AUA growth.

Ongoing Education

Building trust and understanding with members through embedded tools, webinars, employer channels, and expert access.

Growing the Plan

The key add-ons that deepen plan value — match increases, financial planning access, and onboarding integration.

The new standard for plan oversight

The old way

- Compliance as finish line: tick the box, file report

- Emphasis on reviewing investment lineup

- Long reports client doesn't want to read

- Limited visibility into members' retirement health, if benefit it working

The new way

- Focus on outcomes: is the plan actually working?

- Focus on usage & adoption: are employees engaging with and using the plan?

- Real-time plan health data: participation, retirement health, digital engagement

- Advisor as ongoing partner, not annual visitor

What employers should be tracking

A good plan review doesn't need a 100-page fund report. It needs a clear answer to one question: is this plan actually working for our people?

What % of eligible employees are enrolled? Below 70% is a signal that action may be needed (e.g., education campaigns)

Engagement is what makes a plan visible to employees. Invisible benefits don't drive retention.

Common Wealth calculates a Retirement Readiness Score for every member. Employers can see aggregate scores — a powerful proxy for whether the plan is working.

Investment returns matter — but in context. Are members in age-appropriate funds? Are fees reasonable?

What advisors should be tracking

Everything your employer cares about — plus the metrics that tell you whether your book is growing and deepening.

Participation rate

The single best proxy for plan health. Below 75%? Time for a re-enrollment push or auto-enroll conversation with the employer.

Member engagement

Logins, projection views, contribution changes. Engaged members contribute more and stay enrolled longer — both matter to you and to them.

Retirement readiness

The aggregate readiness score across your plans tells you where members need help — and where an education session or CFP referral would have the most impact.

AUA growth rate

Are your plans growing through contributions and returns? A flat AUA book means you're not winning new plans or members aren't increasing contributions over time.

New members & plans

Headcount growth within existing clients is free AUA. New hires who enroll immediately are the easiest members to acquire — make sure onboarding is set up to capture them.

Asset consolidation

Are members rolling outside RRSPs and old workplace plans into your plan? Each consolidation increases AUA and deepens the member's relationship with the plan — and with you.

The advisors who build the strongest GRS books review these metrics quarterly — not just at renewal time. Knowing your numbers lets you have proactive conversations instead of reactive ones.

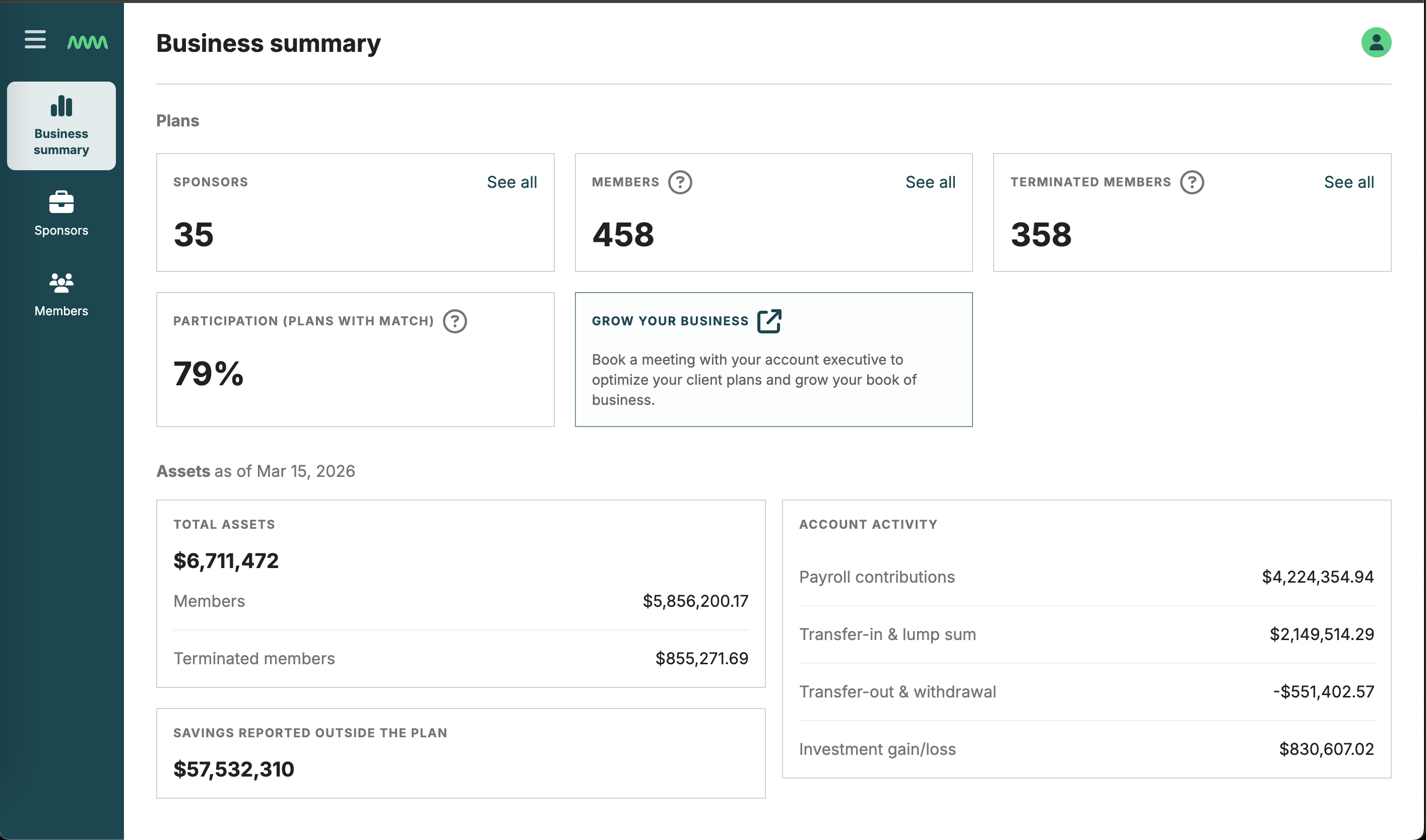

What a plan review looks like

Client-ready simple CAP report available for download directly from Common Wealth Advisor.

Real-time stewardship data in Common Wealth Advisor

How to drive plan performance

Common Wealth's approach to client stewardship

Launching a plan is the start, not the finish. The plans that perform best have an advisor and provider actively working together to keep them growing.

Every plan is assigned a Client Success Manager measured on employer satisfaction and member participation. Advisors can lean on them for client support or let them engage directly on operational questions.

Larger employers get annual governance meetings. Smaller ones get a clean written report they can actually use. The approach fits the client — not the other way around.

SMB employers don't want a data dump. The insights that spark the best conversations: retirement readiness scores, participation rates, transfer-in activity, and investment returns.

Some advisors want robust data and handle client engagement themselves. Others want Common Wealth to take a more active role. The model adapts to fit how you already work.

Trust is built through consistent education

The plans that perform best over time are the ones where members understand what they have, why it matters, and what to do next. That doesn't happen automatically.

Embedded in the product

The most powerful education happens inside the app — at the moment a member is already engaged. Common Wealth surfaces retirement income projections, contribution nudges, and investment guidance in context, without requiring a separate session.

Employee webinars

Live education sessions on retirement-focused topics such as retirement income planning, cash flow and debt management, estate planning, lifestyle and transition planning.

Employer as channel

The employer is your distribution partner for member education. A well-timed internal newsletter, Slack message, or all-hands mention from the CEO drives more engagement than any advisor-sent email. Equip employers with content they can actually use.

Access to human experts

For members with complex situations, access to a Certified Financial Planner (CFP) builds enormous trust. Common Wealth provides member-facing financial planning support — so the advisor handles employer relationships while members get the guidance they need.

The compounding effect: Members who understand their plan contribute more, consolidate outside assets, and stay enrolled longer. Better-educated members = higher AUA = more revenue for you, better outcomes for them.

Four add-ons that deepen plan value over time

The first year of a plan is about getting it right. Year two onward is about making it better. These are the highest-impact conversations to have at annual review.

Increase the employer match

A match increase is the single most effective way to improve participation and contribution levels. Even moving from 3% to 4% signals genuine commitment to employees — and drives immediate behaviour change. Frame it as a compensation decision, not a plan admin one.

Financial planning access

Adding access to a CFP or financial planning tool gives members something most plans don't offer: personalized guidance. Common Wealth's CFP access can be layered onto existing plans. It builds member loyalty, increases engagement, and surfaces consolidation opportunities.

Embed in employee onboarding

New hires who enroll on day one stay enrolled. Work with the employer to add the plan to their onboarding checklist — ideally as a step in their HR system, not an email buried in a welcome package. Auto-enrollment at hire is the gold standard.

Include participation in employment contracts

Some employers take it further: making plan participation a standard part of the employment agreement. This removes any ambiguity about enrollment and signals to candidates that the benefit is real and expected — not optional or overlooked.

Most Canadians don't have a retirement income plan

A group retirement plan is a powerful foundation — but by itself it doesn't answer the most important question members have: will I actually be okay?

of Canadians have a formal written retirement income plan

more investable assets accumulated by those with a written plan

more financial confidence reported by those with a written plan

Financial Planning by Common Wealth

- Certified Financial Planners (CFPs) embedded within Common Wealth — not a third-party referral

- Available as an add-on to any existing group retirement plan

- Members can book sessions directly through the app — low friction, high utilisation

- Advisor-first: the CFP team supports your clients, not replaces your relationship

Differentiators

- Retirement income planning — not just accumulation advice

- Holistic: integrates group plan, personal savings, CPP/OAS, and spending needs

- Written plan delivered to each member

- Ongoing access — members can return as life changes

Expected Impact

- Higher contribution rates post-planning session

- Increased asset consolidation into the group plan

- Stronger employer satisfaction and renewals

- Differentiates your offering from every other advisor in the market

Plans can grow faster with planning

5-year asset projections for a start-up plan with 50 members, 5% match, annual cashflows of $400K

Implementation is the beginning, not the finish line

- The new standard for plan governance is outcomes-first — compliance is the floor, not the ceiling

- Track participation, engagement, and readiness scores — not just investment returns

- Education compounds: members who understand their plan save more, consolidate more, and stay longer

- The highest-impact add-ons are match increases, financial planning access, and onboarding integration

- Your best new clients are already in your book — deepen the relationship before chasing new ones

Advancing retirement plan coverage for small employers

- Advancing proposal to increase retirement plan coverage via a tax credit for small employers

- Would cover cost of setting up a plan and for making matching contributions to employee accounts

- Co-authored policy paper with Keith Ambachtsheer (globally-recognized pension expert) to advance proposal with industry & government stakeholders through C.D. Howe

Connect with your Common Wealth sales team